Choosing the Right Classic Boat Loan for You

Owning a classic boat evokes timeless elegance and adventure on the water. Whether you’re drawn to the polished mahogany of a vintage cruiser or the sturdy fiberglass of a bass boat, financing can make your dream vessel a reality without draining your savings. Classic boats, often defined as those built between 1943 and 1975 by the Antique and Classic Boat Society (ACBS), offer unique charm but come with financing challenges, especially for older models. This comprehensive guide explores classic boat types, financing options, lender restrictions, and practical steps to secure the right loan, with a focus on fishing boats and older vessels in Texas.

Why Choose a Classic Boat?

Classic boats combine nostalgia, craftsmanship, and affordability compared to modern yachts, which can cost $70,000–$90,000 for new models. Older boats, particularly those from 2000 onward, often use durable composite materials, eliminating issues like wood rot prevalent in pre-1990s designs. For anglers or leisure seekers with imperfect credit, classic boats offer value and accessibility, especially through specialized lenders who cater to this niche market.

A day on a classic boat—whether fishing, cruising, or relaxing with loved ones—promises unmatched serenity. However, financing these vessels requires navigating lender hesitations, age restrictions, and credit considerations. Let’s dive into the types of classic boats, their specifications, and how to finance them effectively.

Popular Classic Boat Types

Classic boats vary in design and purpose, each offering distinct advantages for fishing, cruising, or recreation. Below are five popular types, their specifications, and estimated price ranges for used models (2000 or newer where applicable).

| Boat Type | Length | Beam | Draft | Displacement | Hull Material | Used Price Range | Key Features |

|---|---|---|---|---|---|---|---|

| Bass Boat | 16–22 ft | 7–8 ft | 1–2 ft | 1,500–2,500 lbs | Fiberglass/Aluminum | $15,000–$40,000 | Low profile, casting platforms, trolling motor |

| Aluminum Ski Boat | 16–20 ft | 6–7 ft | 1–2 ft | 1,000–2,000 lbs | Aluminum | $10,000–$30,000 | Lightweight, ideal for watersports |

| Cabin Cruiser | 25–35 ft | 8–12 ft | 2–4 ft | 6,000–12,000 lbs | Fiberglass | $30,000–$80,000 | Kitchen, beds, stable in rough waters |

| Broads Yacht | 20–30 ft | 7–10 ft | 2–3 ft | 4,000–8,000 lbs | Fiberglass/Wood | $20,000–$50,000 | Lift-up roof, compact yet spacious |

| Pontoon Boat | 18–28 ft | 8–10 ft | 1–2 ft | 2,000–4,000 lbs | Aluminum | $15,000–$45,000 | Ample seating, 360° view, storage |

Bass Boat

Bass boats are ideal for freshwater anglers, offering open decks and low profiles for easy casting. Equipped with powerful outboard engines (50–150 hp) and quiet trolling motors, they ensure speed and precision. Platforms at the bow and stern double as casting areas or seating for relaxed fishing trips.

Aluminum Ski Boat

Perfect for watersports, aluminum ski boats are lightweight and durable, making them excellent for towing skiers or wakeboarders. Their compact size suits small groups, and their affordability appeals to families recreating nostalgic lake outings.

Cabin Cruiser

Cabin cruisers provide luxury and comfort, featuring amenities like kitchens, toilets, and sleeping quarters. Stable in choppy conditions, they’re suited for overnight trips or entertaining, with engines (100–300 hp) balancing power and efficiency.

Broads Yacht

With a vintage aesthetic, Broads Yachts are compact yet versatile, ideal for solo or small-group outings. A lift-up coach roof expands interior space, making them suitable for fishing or leisurely cruises on calm waters.

Pontoon Boat

Pontoon boats maximize seating and storage, perfect for social gatherings or family outings. Their stable, flat design supports swimming, sunbathing, or picnicking, with engines (40–115 hp) offering moderate speed for lake or river use.

Challenges of Financing Classic Boats

Financing older boats, especially those over 15–20 years old, poses challenges due to lender concerns about depreciation, condition, and resale value. Here’s why lenders hesitate and how these issues impact loan terms.

Why Lenders Avoid Older Boats

- Depreciation: Older boats lose value faster, reducing collateral security if the loan defaults.

- Condition Risks: Wear, outdated systems, or structural issues increase maintenance costs and risks.

- Resale Difficulty: Repossessed older boats are harder to sell, especially unique or vintage models.

Lenders often impose restrictions, such as:

- Age Limits: Many won’t finance boats older than 15–20 years.

- Higher Interest Rates: Rates for older boats range from 10.5% to 16%, compared to 7–10% for newer models.

- Lower Loan-to-Value (LTV) Ratios: Lenders may finance only 60–70% of the boat’s value.

- Mandatory Surveys: A professional marine survey is required to assess condition and value.

Comparison: Newer vs. Older Boat Financing

| Aspect | Newer Boats (Post-2010) | Older Boats (2000–2010) |

|---|---|---|

| Interest Rates | 7–10% | 10.5–16% |

| Loan Term | 15–20 years | 5–10 years |

| Down Payment | 15–20% | 20–30% |

| LTV Ratio | 80–90% | 60–70% |

| Approval Time | 1–2 days | 3–7 days |

| Maintenance Costs | Lower | Higher |

Older boats are more affordable upfront but require larger down payments and incur higher maintenance costs (approximately 10% of purchase price annually). Newer boats offer warranties and lower rates but come with higher purchase prices.

Tips for Securing a Classic Boat Loan

Securing financing for a classic boat, especially in Texas for fishing boats from 2000 or newer, requires preparation. Here are practical steps to improve your chances of approval.

- Conduct a Marine Survey

A certified marine surveyor assesses the boat’s hull, engine, electrical systems, and market value. A clean survey reassures lenders and supports a higher LTV ratio. Expect to pay $15–$25 per foot for a survey. - Maintain a Strong Credit Profile

A credit score of 500 or higher is often required for specialized lenders, though scores in the 700s secure better rates. Check your score via free services like Credit Karma before applying. - Save for a Larger Down Payment

A 20% down payment (minimum $4,000 in Texas) reduces the loan amount and signals commitment. For a $25,000 boat, plan for $5,000 plus 8% TTL (taxes, title, licensing), totaling $6,000 upfront. - Work with Marine-Specific Lenders

Lenders like Classic Boat Loans in Texas or J.J. BEST BANC & CO. specialize in older vessels and offer flexible terms. They understand the marine market and are more likely to finance boats banks reject. - Explore Alternative Financing

If traditional loans are unavailable, consider personal loans, home equity loans, or refinancing other assets. These options may have higher rates but fewer restrictions. - Verify Boat Titles

Ensure the seller holds clear Texas titles in their name. Title issues are common in private sales, so work with a lender to verify ownership before proceeding.

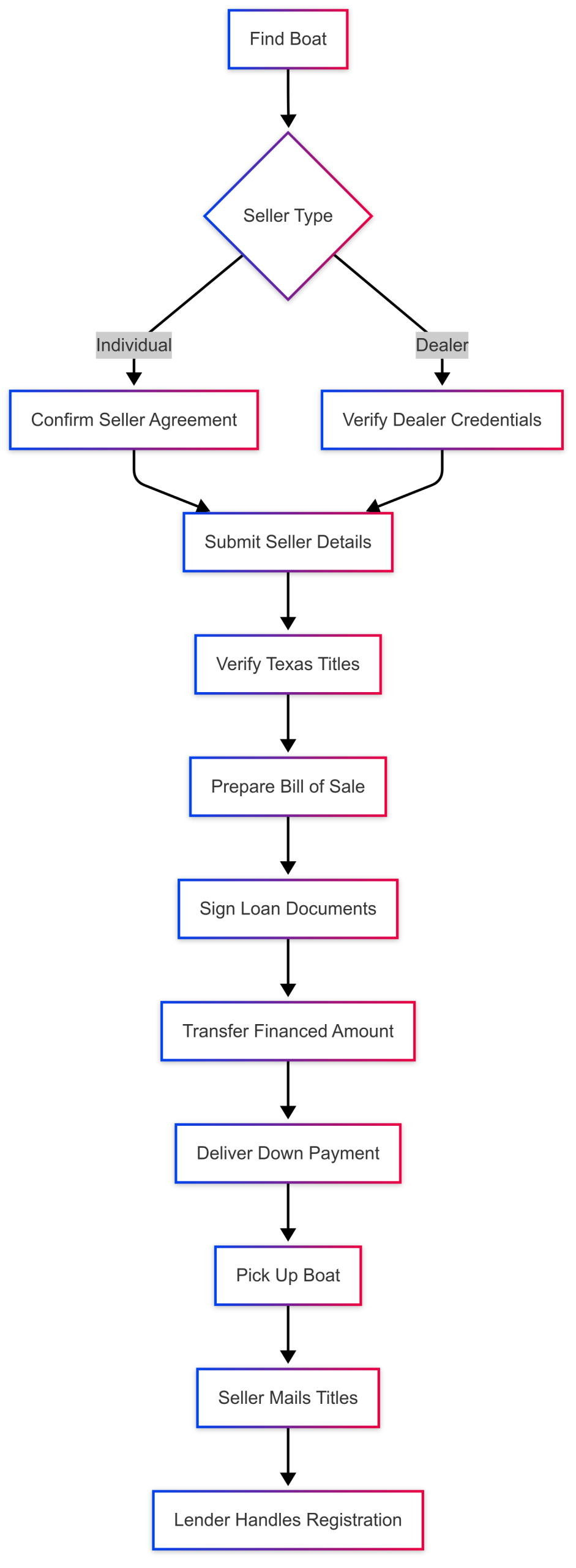

Loan Process for Classic Boats in Texas

Specialized lenders like Classic Boat Loans, regulated by the Texas Office of Consumer Credit Commissioner (OCCC), offer tailored financing for fishing boats from 2000 or newer. Below is the step-by-step process for buying from an individual or dealer.

Buying from an Individual

- Confirm Seller Agreement: Ensure the seller is willing to work with your finance company. Provide a $200 non-refundable deposit to hold the boat.

- Submit Seller Details: Send the seller’s contact information to the lender to verify Texas titles in the seller’s name.

- Bill of Sale: The lender prepares a bill of sale outlining the negotiated price, payment method, and pickup details.

- Loan Documents: Review and sign industry-standard loan documents electronically. Mail originals to the lender.

- Funds Transfer: The lender transfers the financed amount to the seller. You deliver the down payment (cash or agreed method) upon pickup.

- Title Transfer: The seller mails titles to the lender, who handles registration and transfer.

Buying from a Dealer

The process is similar, but the dealer manages title registration. Ensure the dealer is Texas-based and the boat meets lender criteria (2000 or newer, $18,000+ purchase price).

Lender Requirements

- Texas resident for 2+ years

- 2+ years in current occupation (or related field)

- Established bank account for 2+ years

- Credit score of 500+

- Automatic monthly payments from bank account

- 20% down payment + 8% TTL (minimum $4,000)

- Loan value: $15,000–$60,000

- Boat: 2000 or newer, fishing boat, $18,000+ purchase price, Texas titles

Interest Rates and Terms

Classic Boat Loans offers rates starting at 10.5%, adjusted based on your self-reported credit score. Terms range from 48 to 60 months, with no rates exceeding 17.95%, unlike secondary market lenders. For a $25,000 loan at 10.5% over 60 months, expect monthly payments of approximately $550.

Chart: Loan Process Flow

Benefits of Specialized Lenders

Unlike banks, which prioritize newer boats, specialized lenders like Classic Boat Loans and J.J. BEST BANC & CO. focus on older fishing boats and borrowers rebuilding credit. Benefits include:

- Flexible Terms: Loans for boats as old as 2000, with exceptions for older models.

- Lower Rates: Starting at 10.5%, compared to 17.95%+ in secondary markets.

- Fast Approvals: J.J. BEST BANC & CO. approves loans in as little as 2 minutes.

- Expertise: Lenders with marine industry knowledge streamline the process.

J.J. BEST BANC & CO., a major player in wooden boat financing, offers loans from $10,000 to $4 million with terms up to 20 years. Their low rates and penalty-free prepayment make them ideal for classic wooden boats, though they also finance fiberglass and aluminum vessels.

Current Lending Climate

Boat loan interest rates have risen due to inflation, averaging 7–10% for newer boats and 10.5–16% for older ones. Down payments typically range from 15–30%, with zero-down options rare and reserved for exceptional borrowers. Loan terms of 15–20 years are standard, but shorter terms (5–10 years) are common for older boats to mitigate risk.

The Boat Trader Boat Loan Calculator can estimate monthly payments. For a $30,000 loan with a 20% down payment ($6,000) at 10.5% over 60 months, monthly payments are approximately $660. Variables like credit score, boat age, and lender policies affect final costs.

Additional Costs of Boat Ownership

Beyond the purchase price, consider ongoing costs:

- Maintenance: 10% of purchase price annually (e.g., $2,500/year for a $25,000 boat).

- Insurance: $300–$1,000/year, depending on boat value and coverage.

- Mooring/Storage: $500–$5,000/year, based on location and facilities.

- Survey Fees: $15–$25/foot for initial and periodic inspections.

- Taxes and Registration: 8% TTL in Texas, plus annual fees.

Factoring these into your budget ensures you can afford both the loan and ownership responsibilities.

Case Study: Financing a 2005 Bass Boat

Imagine you’re a Texas resident eyeing a 2005 bass boat listed for $22,000 from a private seller. Your credit score is 620, and you’ve been at your job for three years. Here’s how the process unfolds with Classic Boat Loans:

- Down Payment: 20% ($4,400) + 8% TTL ($1,760) = $6,160.

- Loan Amount: $17,600 ($22,000 – $4,400).

- Interest Rate: 11% (based on credit score).

- Term: 60 months.

- Monthly Payment: ~$390.

- Process: You verify titles, sign loan documents, and pick up the boat after funds transfer. The lender handles registration.

A marine survey ($400) confirms the boat’s condition, and you budget $2,200/year for maintenance and $500/year for insurance. This affordable setup lets you enjoy fishing without breaking the bank.

Red Flags to Avoid

- Unclear Titles: Verify Texas titles to avoid legal issues.

- Liveaboard Restrictions: Lenders may hesitate if the boat is your primary residence.

- Charter Use: Commercial use often requires specialty lenders.

- Overlooking Costs: Account for maintenance, insurance, and mooring fees.

- High-Rate Lenders: Avoid secondary market rates starting at 17.95%.

Conclusion

Financing a classic boat, whether a bass boat for fishing or a cabin cruiser for family outings, is achievable with the right preparation. Specialized lenders in Texas, like Classic Boat Loans, cater to older fishing boats (2000 or newer) and borrowers with credit scores as low as 500, offering rates from 10.5%. By conducting a marine survey, saving for a 20% down payment, and verifying titles, you can secure a loan that fits your budget. Platforms like Boat Trader provide listings and financing tools to simplify the process.

For wooden classics, J.J. BEST BANC & CO. offers fast approvals and competitive terms. Before committing, use a loan calculator to estimate payments and budget for maintenance (10% of purchase price annually). With careful planning, you’ll soon be cruising the waters in your timeless vessel, creating memories that last a lifetime.

Happy Boating!

Share Choosing the Right Classic Boat Loan for You with your friends and leave a comment below with your thoughts.

Read Caravan Boats: The Ultimate All-Terrain Adventure Vehicle until we meet in the next article.